The Spanish tax system is much like other European countries in generic terms. Tax in Spain comes in the form of income, capital, property, and inheritance taxes; local taxes vary depending on your circumstances. There are particular distinctions made between resident and non-resident taxpayers. One crucial difference is that each of the 17 autonomous regions in Spain set their rates which are payable in addition to national taxes.

{kind=link}

Spanish residents pay tax on their assets worldwide. It is, therefore, necessary to pay tax on income, capital, and other assets annually. There are exemptions available for temporary workers and Expats. For those who are exempt, the authorities will only tax Spanish sourced income. Individuals who spend 183 days or more in Spain are obliged to declare their worldwide income there.

Brexit and its impact on tax in Spain

After the withdrawal agreement implementation period, UK nationals who are non-resident in Spain will be liable for higher rates of tax on Spanish assets. These apply to:

- Rental property income

- Royalties

- Income from employment

- Deemed income tax from properties not rented

- Profits from companies without a permanent establishment in Spain

An example is tax on rental income from properties, which is 19% for EU residents and 24% for non-EU residents.

Personal income tax rates

There are two forms of taxable income in Spain to consider: general taxable income and savings taxable income.

Tax in Spain on savings income

Residents are taxed on their worldwide savings income and non-residents on their Spanish savings income at a fixed rate. The rates for 2020 are as follows:

- €0 – €6,000: 19%

- €6,000 – €50,000: 21%

- Over €50,000: 23%

Savings taxable income includes interest income, dividends, income from life assurance contracts, purchased annuity income, and income from capital gains from the sale/transfer of assets.

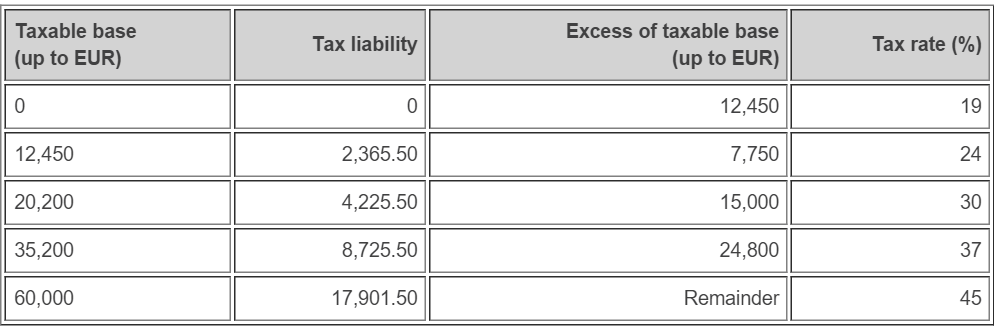

Tax in Spain on general income

Spanish residents pay tax on their worldwide income on a progressive scale. General taxable income includes all income other than ‘savings income’. It covers earned income (that is, salary, self-employment, and pension income), rental income, income from royalties, any capital gains not generated from the sale/transfer of assets such as lottery prizes.

{kind=link}

*Note: Tax rates may differ depending on the region (Comunidad Autónoma) where the taxpayer is resident.

Treatment of UK Pensions

Spanish residents with UK state pensions or occupational pension income are taxable in Spain and not in the UK, under the UK-Spain Double Taxation Treaty. However, UK Government service pensions (e.g. civil service, local authority, fire service, police, and most teachers) remain liable only to UK tax and are therefore not taxable in Spain.

There is a distinction between pensions that are Defined Benefit (DB) and annuity-based. Annuity-based pensions attract considerable tax advantages for those who qualify. Contributions from employers to personal pensions may not benefit in their entirety from the annuity allowance.

Lump sum distributions

In the UK, individuals can take a lump sum of 25% free of tax from their pension on retirement. For Expats, however, any lump sum withdrawn from an overseas scheme is eligible for tax in Spain, irrespective of UK legislation. The system differs in that actual pension contributions are deducted from the lump sum (in proportion to the whole fund). Thereafter, tax on the lump sum is calculated in tranches as follows:

- The first €6,000 is taxed at 20%

- 22% on the remainder up to €50,000

- 24% on amounts over €50,000

Example: an individual takes the full 25% from a €100,000 pot built up with contributions of €60,000. The tax calculation on the lump sum would be:

€25,000 – €15,000 (25% of €60,000 contributions) = €10,000

The total tax due would therefore be:

€1,200 (20% of €6,000) + €880 (€22% of €4,000) = €2,080.

Expats can benefit from Spanish tax planning opportunities. It might be better for those already in the tax system to forgo the lump sum and take a higher annuity income as long as that annuity qualifies for the favourable tax treatment mentioned above. A UK tax resident planning to move permanently to Spain might consider taking the lump sum while it is still tax-free in the UK.

QROPS in Spain

British Expats and other UK pension holders often choose to transfer their funds into a QROPS to benefit from the annuity exemption fully. QROPS offer inheritance and succession tax advantages as the pension is held in trust. The individual does not directly own the assets within the trust; this creates a distance from ownership upon death. Any inheritance from the QROPS can thus be received free of Spanish succession tax.

Wealth Tax in Spain

Wealth tax is payable on total worldwide assets for Spanish tax residents. Allowances are generous; everyone has a personal allowance of €700,000 in addition to €300,000 for their principal residence. The State taxes assets on the value that exceeds the allowance limit on a scale ranging between 0.2% to 2.5%. Levels of taxation vary across the Spanish regions. In Andalucia, for example, rates start at 0.24% and rise on a sliding scale to 3.3%. Before calculating the liability, Spanish tax residents can deduct values related to their pension rights, intellectual property rights, household contents, shares in small businesses, family businesses, and property companies.

Capital Gains Tax in Spain

Capital Gains Tax is payable on the sale or transfer of qualifying assets. Rates are in line with savings income tax rules. Liability depends on which asset sales qualify and which don’t. Exemptions are available according to each individual’s circumstances.

Property Tax in Spain

Expats in Spain are also eligible to pay property taxes. Spanish VAT (IVA), document fees, and sales transfer taxes (similar to UK stamp duty) are payable. The rates vary according to what type of property is purchased, the value, and the region. Additionally, everyone pays a local property tax similar to the UK’s council tax.

Inheritance Tax in Spain

The government reformed Spanish inheritance tax in April 2019. Several regions in Spain have introduced a discount of 99% on inheritance and gift tax liabilities. There is a €1m tax-free exemption which means that anyone inheriting less than €1m will pay zero Spanish inheritance tax. Inheritances over €1m will only be taxed at a nominal 1% rate. Similarly, no charge will be payable on gifts, which compares highly favourably with the previous complex and penal system.

As with most country’s tax systems, assessing liabilities and claiming allowances can be a complicated procedure. In addition to using a financial adviser in Spain, we recommend consulting a qualified accountant.