There are many issues surrounding financial planning and Brexit that expats should be aware of. I’m going to make a bold prediction though. Life will go on even if the UK decides to leave Europe! I don’t say this glibly. History shows that every time major political and economic events rock our world, we can gather ourselves, recover and move forward.

There are many issues surrounding financial planning and Brexit that expats should be aware of. I’m going to make a bold prediction though. Life will go on even if the UK decides to leave Europe! I don’t say this glibly. History shows that every time major political and economic events rock our world, we can gather ourselves, recover and move forward.

Brexit has, of course, dominated the news of the last few years; predictions of the future vary from sunlit uplands to complete disaster. The truth will most likely be found somewhere in between. There will be a period of adjustment and things will certainly change. However, the extent to which our everyday lives are affected will largely depend on how we prepare beforehand and react afterwards.

For many, the main driver of change will be their tax residence status. Brexit is forcing expats to reconsider their current position, with increasing numbers deciding to become fully resident in their host country’s system. This may bring new challenges; however new opportunities will also be available for those who make the right decisions.

From an expat financial planning perspective, there are several issues we need to think about and address:

1.Financial planning and Brexit: Currency Issues

As expats, how does our currency strategy fit with our financial commitments? If out-goings are predominantly in Euros, we should seek to ensure that our in-comings match this. By the same token, if the balance of our outgoings is roughly 50/50 in Sterling/Euros, it makes sense to manage our currency strategy in a way which reflects this. We have three basic options for consideration:

- eliminate risk by matching our asset and liability position

- make a conscious decision regarding the future value of currencies and understand the risks involved

- create a ‘natural hedge’, whereby we spread our savings and investments around a range of currencies.

2. Financial planning and Brexit: Investment issues

In the same way that we need to create a currency strategy, we should also ensure that our investments are managed in the most tax-efficient manner possible. They should also accurately reflect our appetite for risk. Issues such as the capacity for loss, the length of time we intend to invest and how our circumstances might change should be considered carefully before investing.

All flavours of investment funds are available globally; we must always be wary of ‘one size fits all’ solutions. Equally, funds which contain lock-in periods should be treated with a healthy dose of scepticism. It’s always easy to get into such funds, but difficult to get out if things go wrong.

3. Financial planning and Brexit: Tax issues

Tax planning is a vital element of anyone’s financial strategy. Each constituent should be viewed in terms of the impact on our tax position. A change in residence can mean that previously tax-effective arrangements become taxable in the new environment. A classic example of this is the tax treatment of UK ISAs for those residing in France or Spain. Instead of continuing to roll-up tax-free, they would become liable to Capital Gains Tax and, potentially, Savings Income Tax.

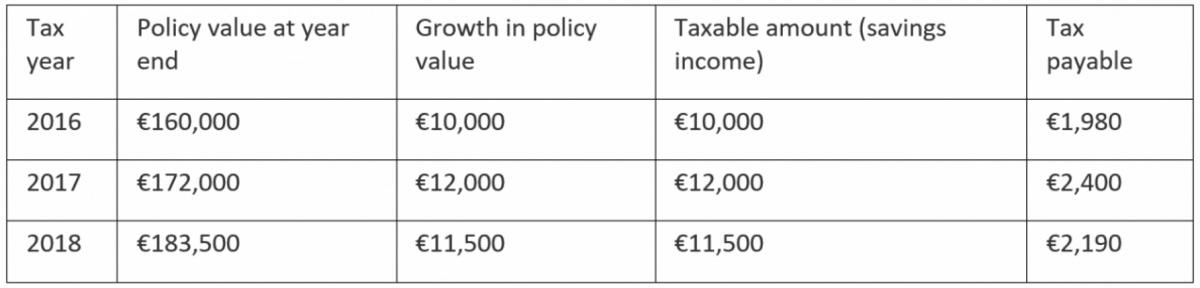

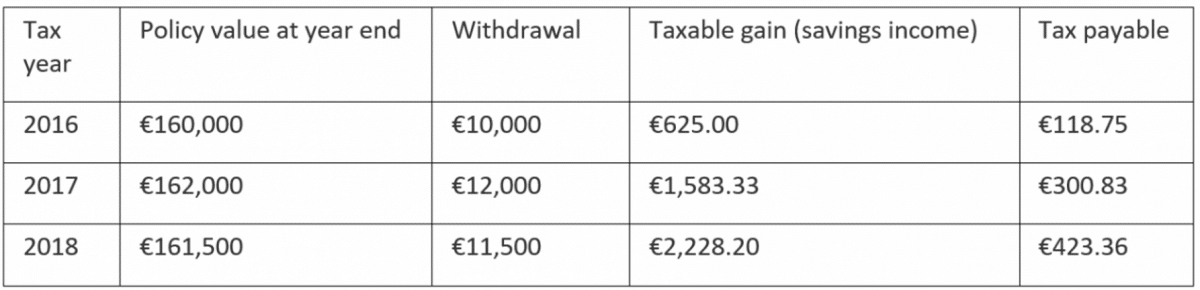

Thankfully, solutions exist whereby we can change the structure of our investments to retain tax benefits. The tables below show the difference in the tax treatment of ‘non-compliant’ and ‘compliant’ investments in Spain.

Non-Compliant investments

Compliant investments

4. Financial planning and Brexit: Pensions issues

Pension plans are fast becoming the largest single investment we ever make; they often overtake the cost of our properties. All of the above issues need to be considered when creating our pension planning strategy. Making sure that we use the most effective structure, the most appropriate investment portfolio, and take advantage of tax concessions are all vital components of pension planning. You should also not overlook the effect of currency decisions when designing a strategy. UK state pensions took a 20% hit just after the Brexit referendum due to the devaluation of Sterling. Nothing can be done to protect ourselves from such a situation occurring; however, we do have full flexibility in the management of our pensions and related investments.

In conclusion, change is certainly coming. Our reaction to this change will decide just how robust and effective our strategy will be in terms of financial planning and Brexit. Flexibility is hugely important. Taking full advantage of local and international tax-efficient investment plans can in some cases be a ‘no brainer’. We must always ensure that our pension planning fits our lifestyle requirements and also that it will outlive us.