As QROPS advisers, we are often asked how much a pension transfer costs and how long a pension transfer takes. It may come as a surprise for some, but the daily life of a financial adviser isn’t all fast cars, glamourous locations, and champagne lifestyles (Ho ho!). Pension transfers are a relatively complex administrative procedure, where attention to detail is paramount, and a little persistence is often required.

How long does a pension transfer take?

Administration and security procedures have to be precise when transferring a UK pension to a QROPS. The first thing we need to establish is how each pension provider operates. There is no ‘one size fits all’ approach, as all providers differ in some way from each other.

The first step is to request an illustration and full QROPS transfer pack. In an ideal world, all providers would be happy to use encrypted email to communicate with advisers. However, there are still some who insist on using ‘snail mail’ for all correspondence. This can create issues in certain countries whose postal systems aren’t as efficient as we’d like. Similarly, some providers will accept a ‘Letter of Authority’ (LoA) by email to begin the process. Others won’t, and some don’t even accept LoA’s from advisers. Our job, therefore, is to know as much as possible in advance about how each company operates.

The first step is to request an illustration and full QROPS transfer pack. In an ideal world, all providers would be happy to use encrypted email to communicate with advisers. However, there are still some who insist on using ‘snail mail’ for all correspondence. This can create issues in certain countries whose postal systems aren’t as efficient as we’d like. Similarly, some providers will accept a ‘Letter of Authority’ (LoA) by email to begin the process. Others won’t, and some don’t even accept LoA’s from advisers. Our job, therefore, is to know as much as possible in advance about how each company operates.

By having a bank of knowledge about pension providers’ administration requirements, we can reduce timeframes and costs, which ultimately benefits our clients. Dealing with large companies can be a trial these days as we wade our way through the various telephone options and wait for someone to be available. Knowing how to short-cut the system not only helps save time but cuts down the time taken listening to some tedious pop singer wailing about lost loves!

When we have all of the relevant information, the next stage is to complete the various application and HMRC forms. Our clients then need to sign a ‘discharge’ form for their scheme, which authorises the transfer to the QROPS provider, the application form for the QROPS, HMRC forms and, in some cases, the investment provider’s form. QROPS providers have upped their game recently; most applications can now be completed online. ‘Wet’ signatures aren’t always required as technological solutions exist, which enable this part of the process to avoid printing, scanning, and posting. Similarly, investment providers are also moving into the technological age; many can now accept applications entirely online. This is a welcome development; we expect this to be improved even further in time.

Our view is that any provider who doesn’t embrace technology will fall behind the pack; those who do will be the most successful. Technology saves time and expense, which can only be good for our clients.

How much does it cost?

Competition is also very healthy in the QROPS world. We’ve seen QROPS fees fall significantly in recent years. Not that long ago, a typical pension transfer cost would be £2,000 to establish the QROPS and annual trust fees of £1,500 per annum. The standard pension transfer cost is now more in the region of £800 set up and £1,000 p.a. Some providers even waive the initial fee to secure business and get ahead of their rivals. Our job is to research all available providers individually for each client.

Investment management fees also vary considerably. Investment managers have been in the firing line recently for over-charging on some of their funds. They are supposed to manage portfolios actively. However, research has found many follow an index and still charge high fees. Exchange-Traded Funds (ETFs) are becoming more popular for those who aren’t looking to trade their pension portfolios actively and prefer to follow a series of indices. A typical UK Equity fund might charge in the region of 1-1.5% per annum, whereas an ETF would be around 0.25-0.75% p.a. A significant cost-saving!

Investment management fees also vary considerably. Investment managers have been in the firing line recently for over-charging on some of their funds. They are supposed to manage portfolios actively. However, research has found many follow an index and still charge high fees. Exchange-Traded Funds (ETFs) are becoming more popular for those who aren’t looking to trade their pension portfolios actively and prefer to follow a series of indices. A typical UK Equity fund might charge in the region of 1-1.5% per annum, whereas an ETF would be around 0.25-0.75% p.a. A significant cost-saving!

Every person has differing requirements, of course. Only after an in-depth assessment of risk tolerance and profiling can the most suitable portfolio be created. Some desire access to the widest range of funds available globally. However, others prefer good-quality general funds which don’t need too much daily management. In the latter case, it is usually true that by restricting choice a little, a better deal can be found without compromising quality. Significant savings can therefore be achieved.

QROPS providers take care of ensuring that the transfers from each pension company are completed quickly and efficiently. All administration documents are sent to them. They, in turn, liaise with the pension providers and secure the client’s funds in their QROPS account. It is important to note that transfers are made directly from the pension company to the QROPS provider. Additionally, specialist currency exchange companies take care of the banking element, which achieves significant cost savings. Normal bank exchange rates are typically 3-5% worse than can be secured by a specialist.

Finally, when all monies have been received, funds are transferred to the investment provider to establish the initial portfolio allocation. Safe-guards exist whereby the trustees and investment providers check selections to ensure our client is investing within his/her risk profile. Again, security is paramount, and the combined efforts of ourselves, the QROPS provider, and the investment platform ensure fund selections are made in regulated territories and not in esoteric sectors.

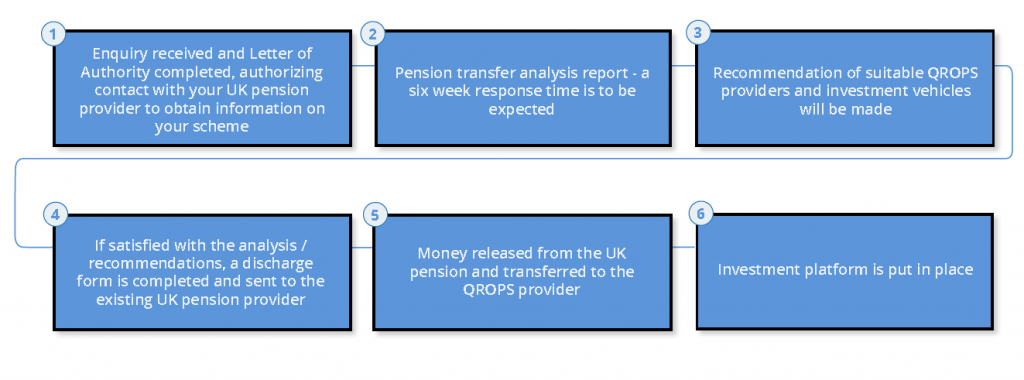

Axis Consultants will act as your facilitator during the QROPS transfer process. Our role is to act on your behalf to gather the necessary information, administer the documentation, and monitor the progress of the transfer. The process generally involves the following tasks:

In conclusion, although the process might appear a little daunting, using the services of experienced professional advisers can make the whole thing a lot easier, not to mention better value.